Enterprise value and equity value are used in various valuation methods. The first step in valuation is to usually obtain the enterprise value or the equity value to arrive at the deliverable, which will be the range of values using various valuation methods. In this article, we are going to discuss the difference between enterprise value and equity value, and which value to use in the appropriate valuation method.

Learning objectives

- Understand what enterprise value is

- Understand what equity value is

Enterprise Value Vs Equity Value

In this article, we’re going to break down the enterprise value and equity value of a business with an illustration for you. The value of a company is a sum of all of its assets. Those assets are used to generate cash flow and they are what the business is actually worth. That’s what’s known as the enterprise value, the value of the entire firm, the value of the entire enterprise.

But a company has a capital structure, those assets were purchased or financed with a combination of debt and equity. So on the other side of this diagram, we’re going to show you how capital structure impacts what these shareholders own.

Let’s suppose these assets were financed 25% with debt and 75% with equity capital. What that means is, after deducting what the debt investors have helped to finance, you have what’s leftover for the shareholders. So, what’s left to the shareholders is the equity value of the business. And the value of all the assets of the entire company is the enterprise value.

Let’s take another look here at a house example. Imagine three different houses. Each of these houses is financed in its own way. The first house is financed with a $100,000 mortgage and $400,000 equity. The second house is financed with a $400,000 mortgage and $100,000 equity. And finally, the third is financed with a $250,000 mortgage and $250,000 equity. So, the question is, what is the house worth in each of the three cases?

Answer To The Question

It’s actually a trick question because all three are exactly the same. The funding mix for the house does not impact its valuation. Thinking about a home and the mortgage in a home is an easy way to think about enterprise value and equity value. If someone asks you what your home is worth you would typically give them the value of the whole house, the enterprise value. Rarely you would tell them the equity value. In business valuation, we think of it in the same way. If you want to think about what an entire company is worth, then you’re thinking about its enterprise value. If you want to know what just the amount that’s worth for the shareholders is, then that’s the equity value.

Enterprise value has a few other names. It can sometimes be referred to as the firm value. So, whenever you hear firm value, think enterprise value. They’re exactly the same. For short, it can also be called TEV, which is the total enterprise value, or simply EV. Sometimes it can also be called the entity value.

On the equity value side, we can also call it the market capitalization, if it’s a publicly-traded company. Or market cap for short. So, equity value, market capitalization and market cap are all the same thing.

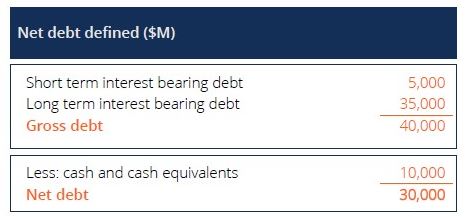

Let’s take a minute to define net debt and understand what the various components of it are. So here’s an example in millions of dollars of calculating a company’s net debt. Take a look at the diagram below.

Here on the balance sheet, this company has a short-term debt of $5 billion, long-term debt of 35 billion, and therefore it has grossed at a 40 billion debt. But netting against that, this company has cash and cash equivalents of 10 billion. Therefore, its net debt is 30 billion.

Important Takeaways

There are two important points to make here about cash in this equation. One is that it is assumed that the cash can be netted against debt that needs to be repaid. So for the reason, you can think about the cash as offsetting the debt because, in a situation where it is required, that cash could be used to pay off. That may not necessarily be a good assumption, but it is a general assumption that is made. The other thing to note is that cash is not an operating asset that generates cash flow for the business. So in that sense, it wouldn’t be included in the asset value of the company or the firm value. So cash is netted out from the total debt to get the net debt.

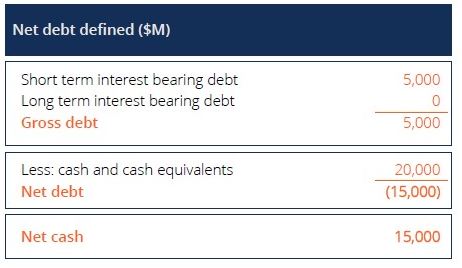

Let’s take at another example of calculating net debt for a company that actually has a positive net cash position, as this can definitely happen. Imagine a company now that has a short-term debt of 5 billion, zero long-term debt and therefore gross debt at 5 billion.

We then need to deduct that from the cash position, that is 20 billion. And therefore, that results in a net debt position of negative 15 billion. We would rephrase that to say it has a net cash position of 15 billion. Going back to our enterprise value calculation or equity value calculation, we would add the 15 billion of cash to the asset value to get the equity value. Or we would deduct the 15 billion of cash from the equity value to arrive at the enterprise value.

Summary

To summarize, the following equations are used to calculate enterprise value and equity value.

Enterprise value = Net debt position + Equity value

Equity value = Enterprise value – Net debt position

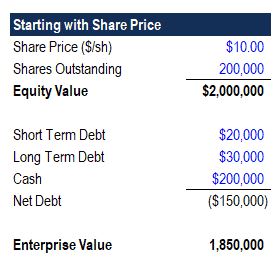

Let’s take a look at the above diagram. We will calculate both the enterprise and equity value in this example.

To calculate the equity value, we’re going to start from the with the share price and shares outstanding. To recap, equity value is the same thing as market capitalization. To calculate equity value, simply take the share price and multiply by the shares outstanding. In this case, the share price is $10 and there are 200,000 shares outstanding. Which means that the equity value is $2 million.

This company has $20,000 short-term debt, $30,000 long-term debt and $200,000 cash. Net debt is calculated as short-term debt plus long-term debt less cash. Result in net debt of negative $150,000. I have purposely made a negative debt because this sometimes can be tricky conceptually. A negative net debt position is also called a net cash position.

Now the enterprise value is going to be the market capitalization plus the net debt. So, in this example, the company has an enterprise value of $1,850,000. What this means is that the assets of the business that are generating the cash flow are worth $1.85 million. The reason that the market capitalization is more than the enterprise value is that there’s a whole bunch of cash on the balance sheet, and that cash is not necessarily generating free cash flow yet, and therefore, it is not included in the enterprise value.

Source: https://www.tianlong.com.sg/enterprise-value-vs-equity-value/